In case you’re constructing a fintech startup in Nigeria, one of many first stuff you’ll want to determine is that this: what CBN licences do we have to function legally, and the way a lot will it price?

Whether or not you intend to launch a digital pockets, a cellular cash app, a financial savings platform, or a full-scale digital financial institution, the Central Financial institution of Nigeria (CBN) requires you to be licenced. And never simply any licence. The sort you apply for will depend on your companies, how you progress cash, and whether or not you’re holding buyer funds.

This information breaks every part down clearly. You’ll study:

- The various kinds of CBN licences accessible

- What every licence means that you can do

- The capital necessities and precise prices concerned

So, what sort of licence does your startup want? Let’s discover out.

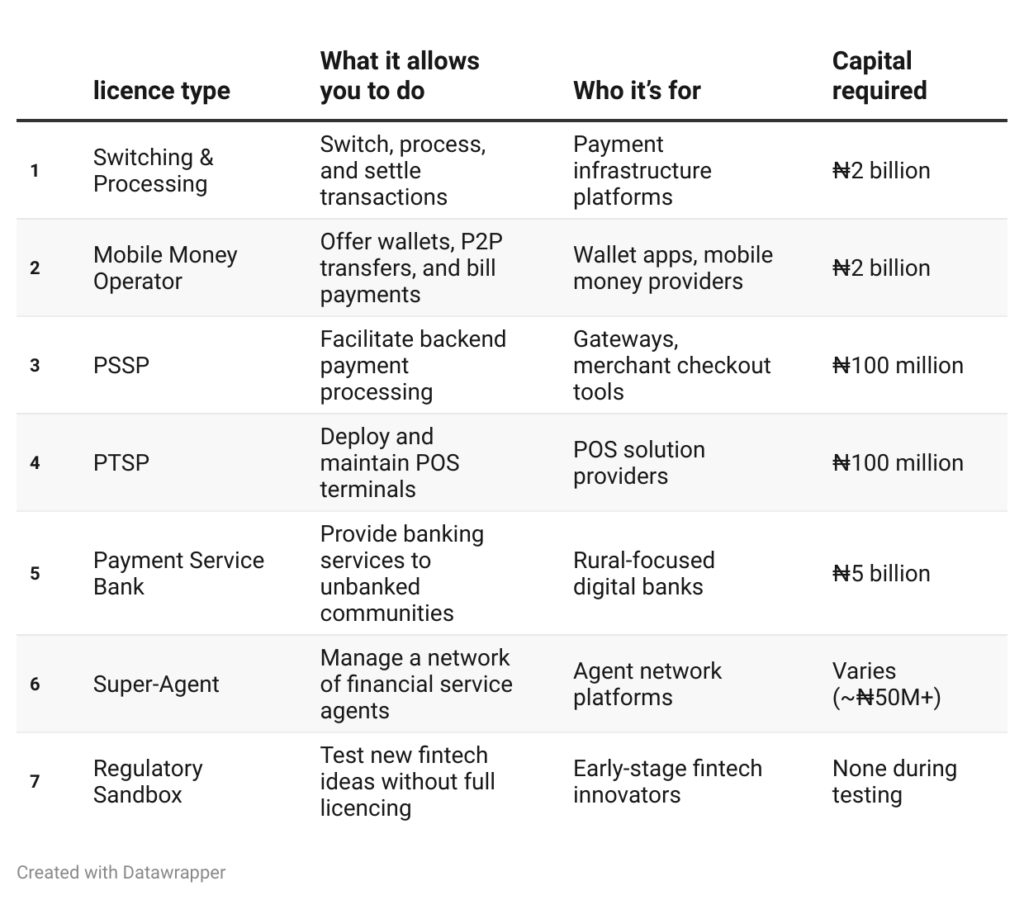

The principle kinds of fintech CBN licences in Nigeria

Earlier than investing time or cash into your fintech product, you could know what licence aligns together with your companies. Beneath are the principle kinds of licences issued by the CBN, what they’re used for, and the sorts of startups that apply for them.

We’ve additionally included capital necessities, so what to anticipate upfront.

1. Switching and Processing Licence

- Who wants this: Corporations that course of funds, settle transactions, or function cost gateways (e.g., Paystack, Flutterwave).

- What it means that you can do: Transaction switching, card processing, clearing, and settlement companies.

- Minimal capital: ₦2 billion

- Different necessities are PCI-DSS certification, a catastrophe restoration plan, danger frameworks, and agreements with banks or retailers.

- Software price: ₦100,000 (non-refundable)

- CBN deposit (escrow): ₦2 billion (returned after the licence is issued)

Is your startup constructing infrastructure that connects banks, wallets, and cost platforms? Then that is doubtless the licence you want.

2. Cell Cash Operator (MMO) Licence

- Who wants this: Pockets-based platforms that enable customers to retailer and switch funds (e.g., Paga, OPay).

- What it means that you can do: Supply wallets, ship/obtain cash, pay payments, and extra.

- Minimal capital: ₦2 billion

- CBN deposit (escrow): ₦2 billion

- Different necessities: 5-year marketing strategy, KYC/AML procedures, information safety insurance policies, and agreements with telcos or banks.

Planning to run a cellular pockets or construct a cash switch app? This licence is necessary.

3. Cost Resolution Service Supplier (PSSP) Licence

- Who wants this: Gateways and APIs that facilitate on-line transactions for different companies (e.g., Remita).

- It means that you can present backend companies for cost processing between banks, retailers, and customers.

- Minimal capital: ₦100 million

- Escrow deposit: ₦100 million

- Further necessities: Card safety certifications, accomplice agreements, strong IT, and danger insurance policies.

In case your startup helps retailers with checkout methods or cost APIs, that is the licence for you.

4. Cost Terminal Service Supplier (PTSP) Licence

- Who wants this: Corporations that handle and distribute POS terminals.

- It means that you can deploy and keep point-of-sale gadgets throughout Nigeria.

- Minimal capital: ₦100 million

- Escrow deposit: ₦100 million

- Key necessities: PCI-DSS/PA-DSS compliance, draft technical agreements, and an in depth venture rollout plan.

Does what you are promoting handle POS terminals or construct POS options? You’ll want this licence earlier than you develop.

5. Cost Service Financial institution (PSB) Licence

- Who wants this: Establishments targeted on offering banking companies to the unbanked and underbanked, typically in rural areas.

- What it means that you can do: Settle for deposits, switch funds, function financial savings merchandise, and situation debit playing cards.

- Minimal capital: ₦5 billion

- Particular requirement: A minimum of 25% of banking brokers should be in rural or underserved areas.

Pondering of launching a digital financial institution that targets financially excluded populations? That is your go-to licence.

6. Tremendous-Agent Licence

- Who wants this: Platforms managing a community of smaller brokers (not essentially customer-facing).

- What it means that you can do: Create and handle an intensive agent community for monetary companies.

- Minimal capital: Varies (typically ₦50 million+ relying on attain)

- Further necessities: Operational construction, danger controls, signed agreements with brokers and monetary companions.

In case you’re constructing a last-mile distribution mannequin utilizing discipline brokers or kiosks, this licence provides you the authorized framework to scale.

7. CBN Regulatory Sandbox

- Who wants this: Early-stage startups testing progressive concepts that don’t clearly fall beneath present CBN licences.

- It means that you can check new monetary merchandise beneath CBN supervision with out full licencing.

- Value: No capital deposit required throughout testing

- Course of: Software-based, with approval timelines of 45–60 enterprise days

Nonetheless determining your mannequin? The sandbox means that you can validate your concept earlier than spending large on a licence.

CBN fintech licence abstract desk

Right here’s a fast desk exhibiting the most typical fintech CBN licences in Nigeria, their use, and the capital required.

What does it price to get a CBN fintech licence?

Getting a licence in Nigeria doesn’t simply imply filling out varieties and ready for approval. It means spending actual cash. In case you don’t funds correctly, the method can stall or fail.

Let’s break down the precise prices it is best to count on.

1. Software charges

These are non-refundable and should be paid to start out your licencing course of.

- Relying on the licence, most utility charges vary from ₦100,000 to ₦500,000.

- Some licences, like Cost Service Banks, might require further administrative or inspection charges throughout the overview stage.

Tip: Don’t confuse this with the capital deposit. Software charges are paid upfront and are separate out of your operational funds.

2. Capital necessities

That is the place it will get critical.

- Switching/Processing and MMO: ₦2 billion (escrow deposit)

- Cost Service Financial institution (PSB): ₦5 billion

- PSSP and PTSP: ₦100 million

- Tremendous-Agent: Varies, however typically ₦50 million or extra

- Digital banks: ₦2 billion+

- Microfinance banks: ₦20 million to ₦100 million (Tier-based)

These quantities are both:

- Held by the CBN throughout processing, then refunded

- Or required as minimal paid-up share capital, that means you could personal the funds and replicate them in your monetary statements.

3. Authorized, compliance, and consulting charges

You’ll doubtless want authorized consultants, compliance advisors, and typically former regulators to overview your paperwork and construction.

- Anticipate to spend ₦2 million to ₦10 million on:

- Authorized counsel

- Drafting partnership agreements

- Creating KYC/AML insurance policies

- Reviewing tax and possession documentation

This is among the most underestimated prices. Slicing corners right here might result in rejection or delays.

4. Tech and operational prices

The CBN needs to see that you just’re able to function. Which means budgeting for:

- IT safety instruments

- KYC software program

- Inside controls and monitoring

- Worker onboarding and coaching

- Knowledge safety insurance policies

- Bodily workplace necessities (for on-site inspections)

Put aside ₦3 million to ₦10 million relying in your scale.

5. Annual renewal and compliance prices

Each licence should be renewed yearly. Renewal charges are decrease than your preliminary licence price however nonetheless important, typically ₦1 million+, relying on the licence kind.

You’ll additionally want to take care of:

- Month-to-month or quarterly compliance experiences

- Common audits

- Ongoing KYC and safety upgrades

What impacts the full price of getting licenced?

Not all fintech startups pays the identical quantity for licencing. Listed below are the important thing components that decide how a lot you’ll must spend:

1. What you are promoting mannequin

- Are you holding buyer funds?

- Are you constructing infrastructure for others?

- Are you issuing playing cards, wallets, or working peer-to-peer companies?

Every of those has totally different licence necessities. For instance:

- A pockets app = MMO licence (₦2 billion)

- A card cost processor = Switching licence (₦2 billion)

- A financial savings and lending platform = Microfinance licence (₦20M–₦100M)

What core service are you providing? Begin there and match it with the required licence.

2. The capital threshold

Some licences require paid-up share capital. Others require escrow deposits that you just’ll get again.

Both means, it’s cash that must be prepared, traceable, and legally yours.

3. Compliance calls for

The extra delicate the monetary exercise, the upper the scrutiny.

- Are you working identification checks?

- Are you stopping fraud?

- Are your buyer data encrypted and safe?

You could must spend money on instruments like:

- KYC/AML compliance software program

- PCI-DSS certifications

- Inside monitoring methods

This provides each upfront and recurring prices to your funds.

4. Documentation high quality

You’ll be requested for:

- A 5-year marketing strategy

- Threat administration framework

- Safety and privateness insurance policies

- Agreements with companions

- Board and shareholder documentation

Poor documentation can delay your utility or result in outright rejection. In case your startup doesn’t have already got these, count on larger consulting charges.

Remaining ideas

You don’t must guess your means by the CBN licencing course of.

By now, the important thing licence varieties, how a lot they price, and what it takes to get authorised. You additionally know the best way to match your product to the proper licence and construct a funds that gained’t depart you stranded midway.

If there’s one factor to remove, it’s this: getting licenced isn’t just a authorized requirement, it’s a development technique. It reveals buyers, prospects, and companions that you just’re critical, compliant, and constructed for scale.

So, what’s your subsequent transfer? If your product, match it to the proper licence. If not sure, begin with a sandbox or seek the advice of a regulatory professional. And should you’re prepared, begin budgeting and constructing your utility. Your fintech concept deserves to launch the best means.

{kind=link}