{kind=link}

An article from

![]()

Dive Transient

//

Financial Studies

A complete of 21 tasks valued at $100 million or extra entered the planning levels in October, together with a $215 million Google information middle, in keeping with Dodge.

Printed Nov. 7, 2023

Connecticut DOT crews reconstruct a southbound I-95 bridge on Nov. 5, 2023, in Westport, Connecticut.

John Moore/Getty Pictures by way of Getty Pictures

This audio is auto-generated. Please tell us when you have feedback.

Dive Transient:

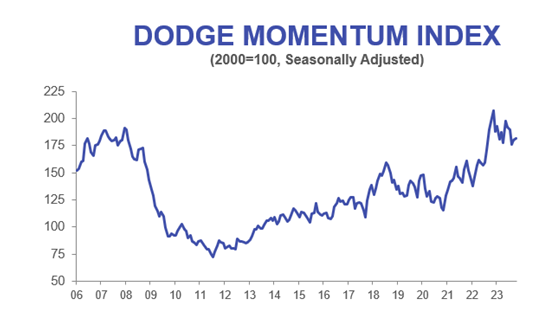

- The Dodge Momentum Index, a benchmark that measures nonresidential constructing planning, inched up 1% in October pushed largely by warehouse exercise, in keeping with the Dodge Development Community. It’s the second consecutive month of constructive good points.

- September’s report reversed six months of contractions. This month’s sequential achieve means that the index, which peaked in December 2022 and sometimes leads precise building spending by 12 months, continued to construct on its constructive route.

- “Heightened momentum in warehouse planning exercise supported the industrial facet of the index this month, whereas muted schooling planning exercise slowed the institutional portion,” stated Sarah Martin, affiliate director of forecasting for Dodge Development Community. “Total ranges of planning exercise stay strong and can help building spending over the subsequent 12 to 18 months.”

Dive Perception:

Martin stated final month that lingering excessive rates of interest, provide chain snarls and tighter lending requirements are more likely to proceed to weigh on the industrial section, corresponding to workplace, retail and warehouse tasks.

So, whereas enhancements in warehouse planning pushed the general industrial element to rise 2% in October, issues stay across the section’s outlook. Yr over 12 months, the DMI for the industrial section stays down 14%, in keeping with Dodge.

On the institutional facet, which incorporates schooling, life sciences and healthcare tasks, the section additionally posted a drop in planning, falling 1.4% in October, in keeping with Dodge. However, the sector as a complete has been largely resistant so far to market headwinds, stated Martin. Yr over 12 months, the institutional section stays up 7%, in keeping with the report.

“Month-to-month motion within the index could be unstable, however 2023 developments proceed to indicate an total lower in industrial tasks, offset by extra institutional tasks getting into the planning queue,” stated Martin. “Business planning has been typically in decline since its peak final November however has begun to stabilize in latest months.”

ABI continues to drop

In the meantime, the Architectural Billings Index, which additionally gives a number one indicator for upcoming building work that’s 9 to 12 months out, continued to deteriorate, in keeping with the newest information from the American Institute of Architects. The ABI rating of 44.8 is the bottom rating reported since December 2020 — through the peak of the pandemic — and signifies that the share of companies reporting declining billings has considerably elevated.

“House owners wish to construct, however inflation is wreaking havoc with monetary proformas and forcing value chopping measures on many industrial tasks in order that they’ll proceed,” in keeping with a 12-person agency within the Northeast referenced within the AIA report, with each industrial and institutional specialization.

In line with Dodge, a complete of 21 tasks valued at $100 million or extra entered the planning levels in October. The most important industrial tasks included:

- The $215 Google information middle in Kansas Metropolis, Missouri.

- The $180 million Mauna Kea Seashore Resort in Waimea, Hawaii.

The most important institutional tasks to enter planning included:

- The $400 million Grand Sierra Resort Area in Reno, Nevada.

- The $267 million renovation to Keller Auditorium in Portland, Oregon.