{kind=link}

This text was contributed by Nimide Fala, Vice President of Consumer Expertise at Zest, and Eytan Messika, Co-founder at Nilos as a part of the Rising Tendencies in Cross-Border Funds: A Progress Information for Stakeholders report authored by Aroghene Favour Ndulu and Paschal Okeke.

For African companies and shoppers, cross-border cost options should nail 4 important issues: velocity, affordability, accessibility, and reliability.

Small companies want money stream, so they need on the spot funds. Think about an SME importing materials from China. If funds are delayed, items get caught, and money stream suffers. Freelancers face the identical situation when ready on worldwide funds.

Affordability can’t be ignored. Excessive charges are a dealbreaker for many. Companies, particularly SMEs, function on tight margins, so each greenback counts. They need reasonably priced options with clear, clear charges and no hidden surprises. A few fintech platforms are fixing this by lowering transaction prices and providing predictable change charges, which makes life simpler for companies.

Accessibility is essential. Not everybody has entry to conventional banks; cellular cash is commonly the go-to methodology in Africa. Options should work the place companies and shoppers are, whether or not by cellular wallets, financial institution transfers, or native brokers. M-Pesa is a good instance. It’s made sending and receiving funds easy, even for micro-businesses in rural areas.

Belief is all the pieces. Companies and shoppers must know their cash is protected, the method is safe, and funds will arrive on time, with no errors and no complications. Fintech platforms can sort out this by investing in fraud prevention and real-time monitoring so customers can confidently ship funds.

Options that get these fundamentals allow progress, construct belief, and make cross-border funds extra seamless.

Bettering velocity and transparency

The answer is brutal simplicity. Most suppliers attempt to construct complicated programs, however the winners might be those that ruthlessly eradicate steps. Suppose early Amazon: one-click ordering labored as a result of it eliminated friction. African funds want their “one-click” second.

Convey blockchain into the image. Blockchain improves velocity and solves the “black gap” downside, the place companies surprise, “The place’s my cash?” It creates a clear, shared ledger that exhibits each switch step.

Transparency additionally means communication. Actual-time monitoring, reminiscent of when monitoring a bundle, builds confidence. Ship on the spot updates by e-mail or an in-app so customers know precisely the place their cost is and when it is going to arrive.

Suppliers should work with native banks, cellular cash platforms, and regional programs to maneuver funds shortly. A world community means nothing if it could’t attain the final mile. Onafriq is a good instance; it has linked immediately with cellular wallets throughout Africa, making certain funds arrive even in distant areas.

Ache factors of SMES in cross-border costs

The most important ache isn’t technical – it’s uncertainty. SMEs can’t predict once they’ll receives a commission or what it’ll value. This unpredictability kills progress. It’s just like what kills most startups: not operating out of cash, however operating out of confidence about cash.

Funds that take days to clear disrupt money stream, provider relationships, and buyer expertise. SMEs don’t have the luxurious of ready. They want funds to maneuver shortly and keep aggressive and agile.

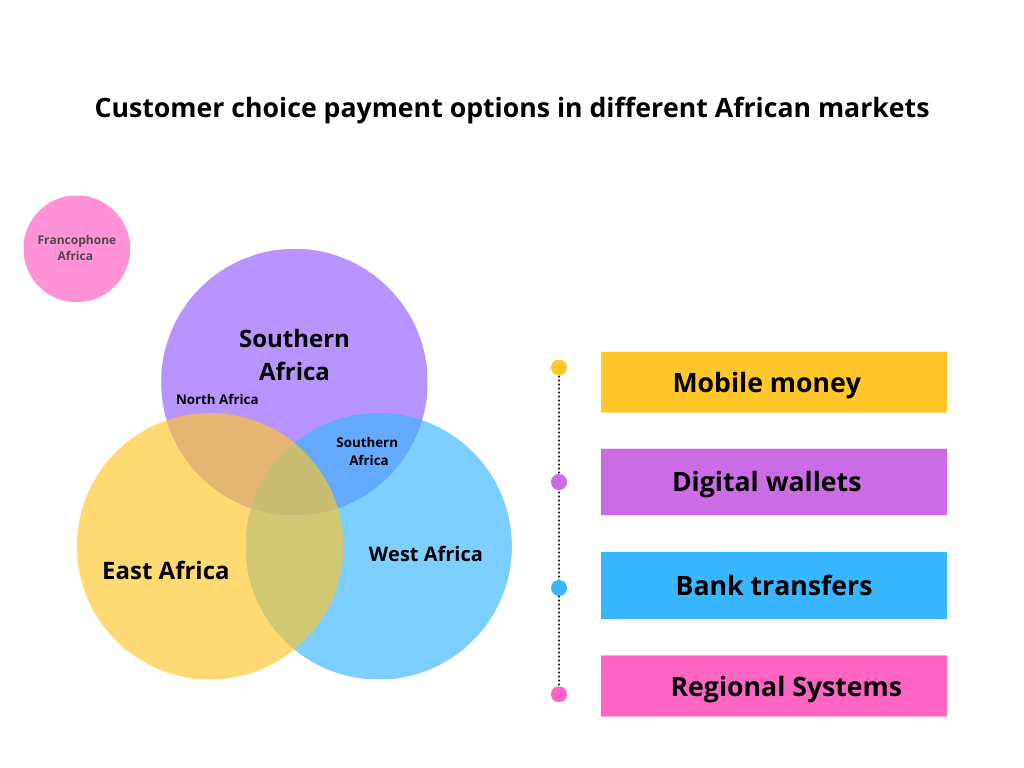

Understanding buyer preferences

East Africa is the heartland of cellular cash, led by pioneers like M-Pesa in Kenya and Tanzania. Cell wallets are king for patrons right here as a result of they’re quick, accessible, and don’t depend on conventional banks. Companies and shoppers typically prioritise instruments that combine with these platforms seamlessly. For instance, a Kenyan service provider receiving funds from Uganda will probably desire M-Pesa-integrated options over financial institution transfers as a result of they’re faster and extra extensively trusted. The cellular cash infrastructure in East Africa is nicely established, and even small distributors in rural areas use it day by day.

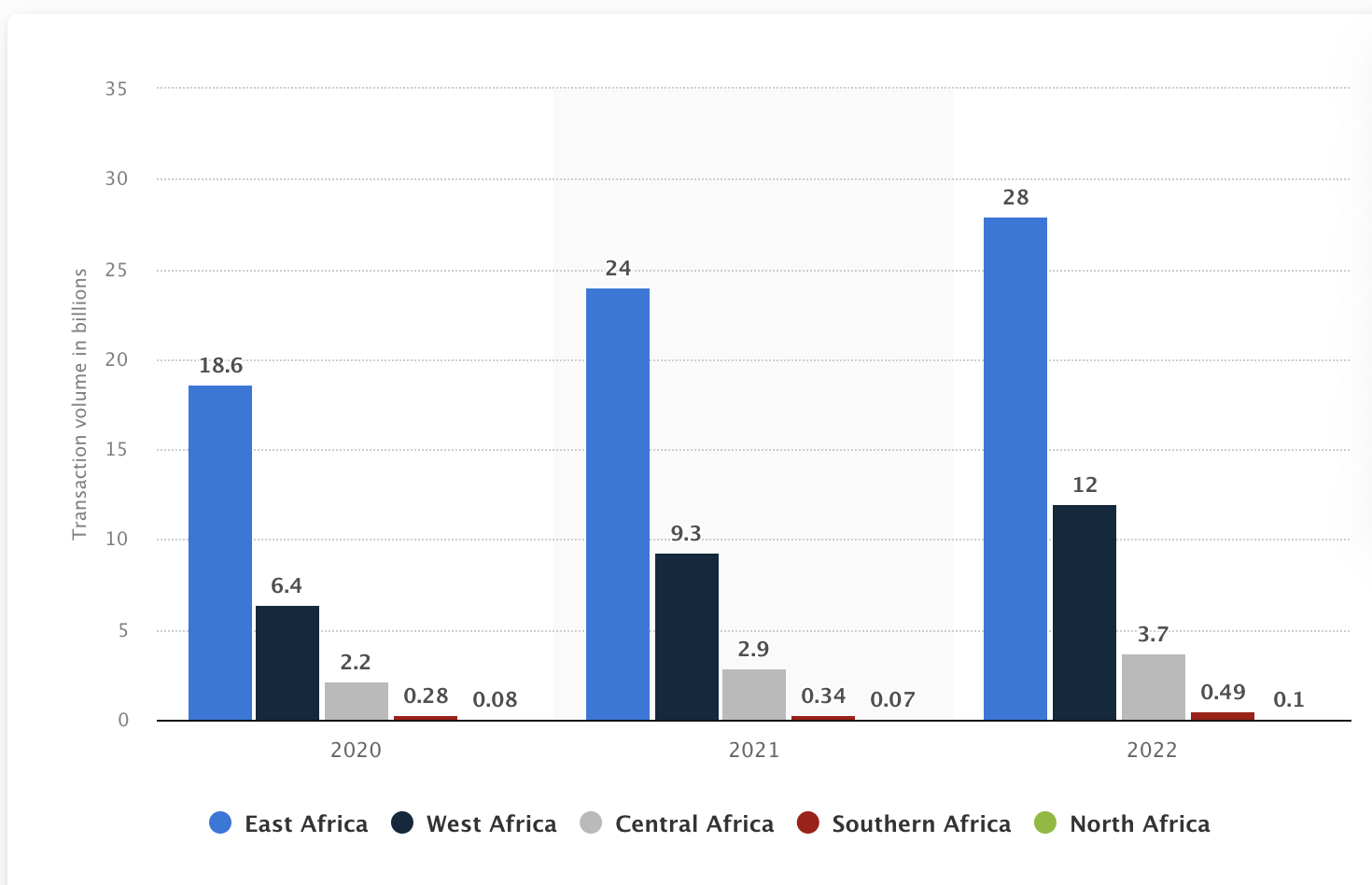

Quantity of cellular cash transactions in Africa in 2020 to 2022 (in billions), by area

Supply: Statistica

Financial institution transfers dominate in West Africa, notably Nigeria. The area depends extra on banks than East Africa, and fintech options are sometimes designed to combine with present banking programs. Nevertheless, money stays important for a lot of casual companies.

Southern Africa, notably South Africa, exhibits a mixture of preferences. Companies and shoppers use digital wallets, financial institution transfers, and card funds. Platforms like Ozow and PayFast are in style for his or her give attention to seamless digital funds, whereas conventional financial institution transfers stay related for bigger transactions. Southern Africa has greater banking penetration and a tech-savvy inhabitants snug with digital wallets and on-line platforms.

Francophone Africa leans closely on regional options like GIM-UEMOA {the interbank cost community) and native digital platforms like Orange Cash. Clients right here prioritise options that work throughout the West African Financial and Financial Union {WAEMU), the place the CFA Franc is shared. A enterprise in Senegal paying a provider in Cote d’Ivoire will typically desire platforms like Wave or Orange Cash for cross-border transfers as a result of they’re quick, reasonably priced, and tailor-made for the area. Regional integration and shared foreign money make it simpler to undertake localised options.

In the meantime, North Africa, Egypt, and Morocco, notably, rely closely on financial institution transfers and the rising use of digital wallets. With robust commerce ties to Europe, companies desire options that bridge native programs with worldwide banking, whereas youthful shoppers are driving digital adoption ahead.

Product and repair localisation in cross-border funds

Product adoption occurs sooner when suppliers tailor their options to native realities like language, foreign money, and most well-liked cost strategies. A platform might need nice options, but when it’s not obtainable within the native language, it turns into a barrier.

Fixed foreign money conversions and reliance on US {dollars} add friction and prices. When companies will pay and receives a commission of their native foreign money, it simplifies operations, cuts prices, and builds confidence to transact globally. It is usually essential to combine native cost choices to ease buyer adaptability.

The perfect localisation is about becoming into present behaviour patterns. M-PESA succeeded as a result of it matched how Kenyans already dealt with cash. That’s the important thing: construct round present behaviours, don’t attempt to change them.

You possibly can learn the complete report right here.

__________________

Nimide Fala is the Vice President of Consumer Expertise at Zest, a fintech subsidiary of Stanbic IBTC Holdings. She is keen about mixing creativity and knowledge for compelling storytelling and designing and executing efficient product and data-led multi-media advertising and marketing methods that drive enterprise and income progress. Her over 13 years of expertise is layered with confirmed information of success for established manufacturers and startups reminiscent of Softcom Africa, Purple Media Africa, Decagon Institute, and so on.

Eytan Messika is the co-founder of Nilos, a fintech startup established in 2021 that gives a platform for companies to unify their crypto wallets, financial institution accounts, and cost service suppliers, streamlining treasury operations throughout each crypto and fiat currencies. He’s a seasoned entrepreneur and monetary expertise innovator with a background in each utilized arithmetic and enterprise technique.