{kind=link}

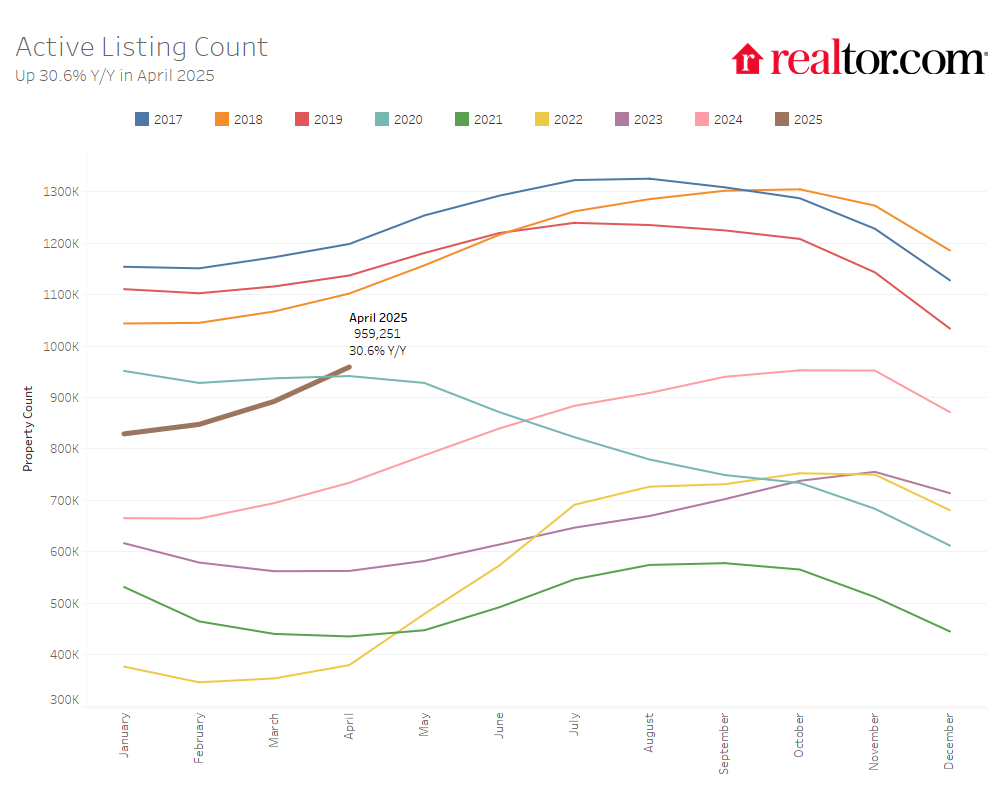

- The stock of houses on the market rose 30.6% year-over-year, marking the 18th consecutive month of stock development. Stock surpassed April 2020 ranges–hitting a brand new post-pandemic excessive.

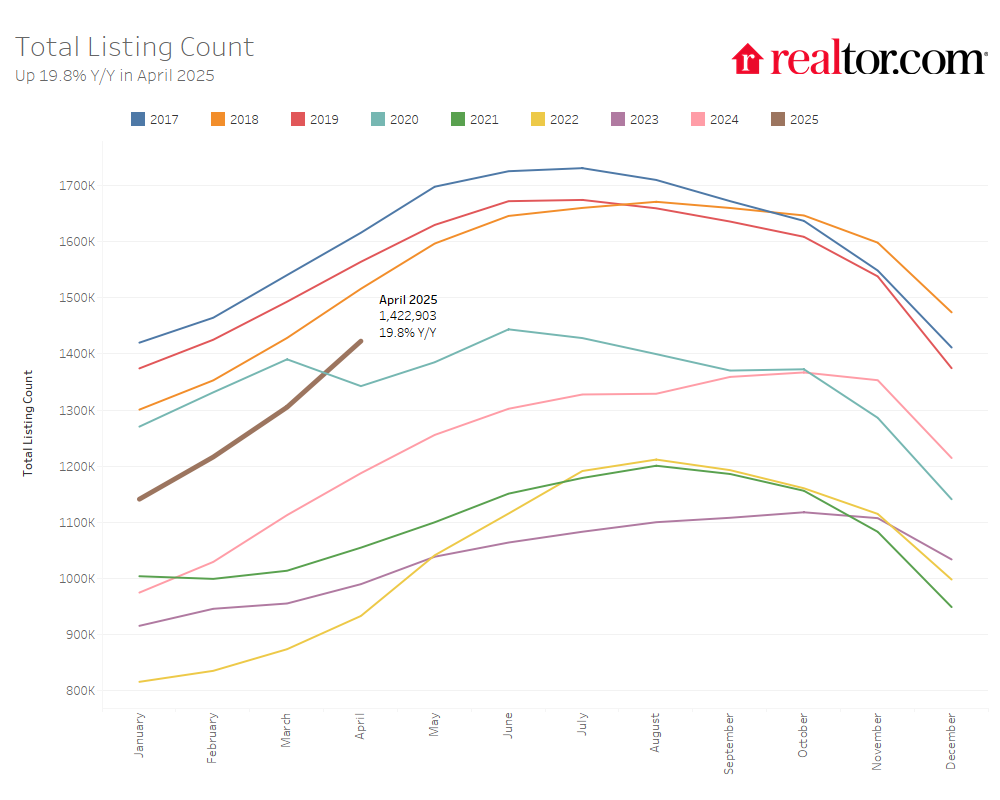

- The complete variety of unsold houses, together with these beneath contract, was up 19.8% in comparison with final 12 months.

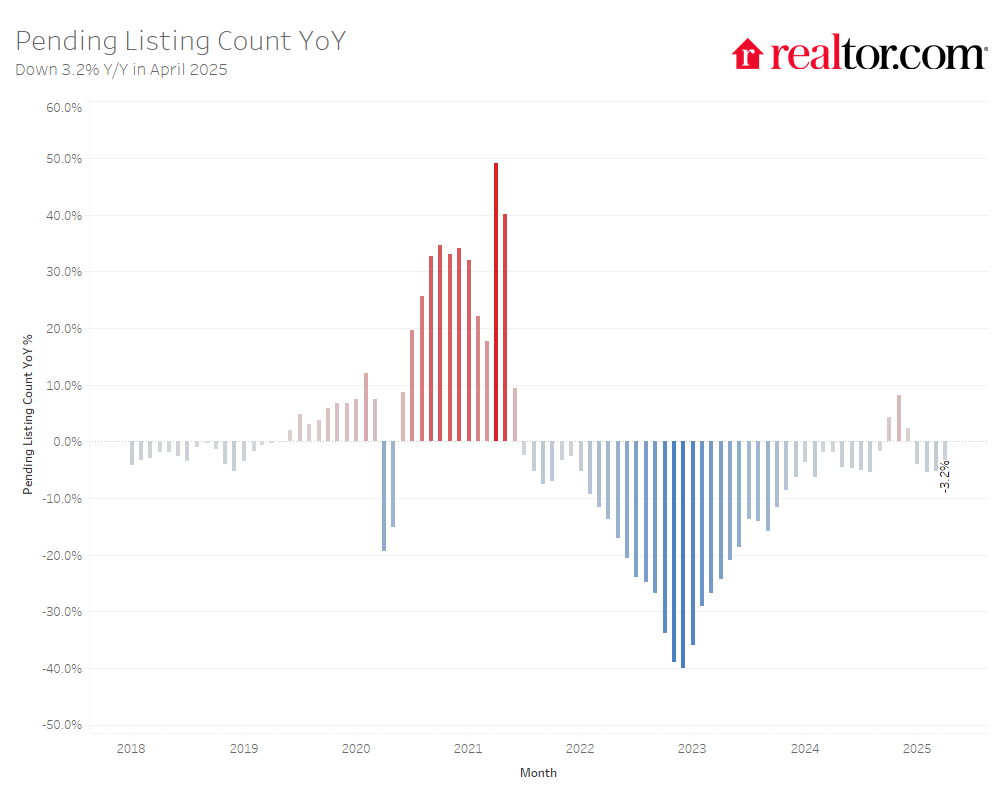

- Pending residence sales- houses beneath contract- fell 3.2% in comparison with final 12 months, as a renewed climb in mortgage charges weighed on consumers.

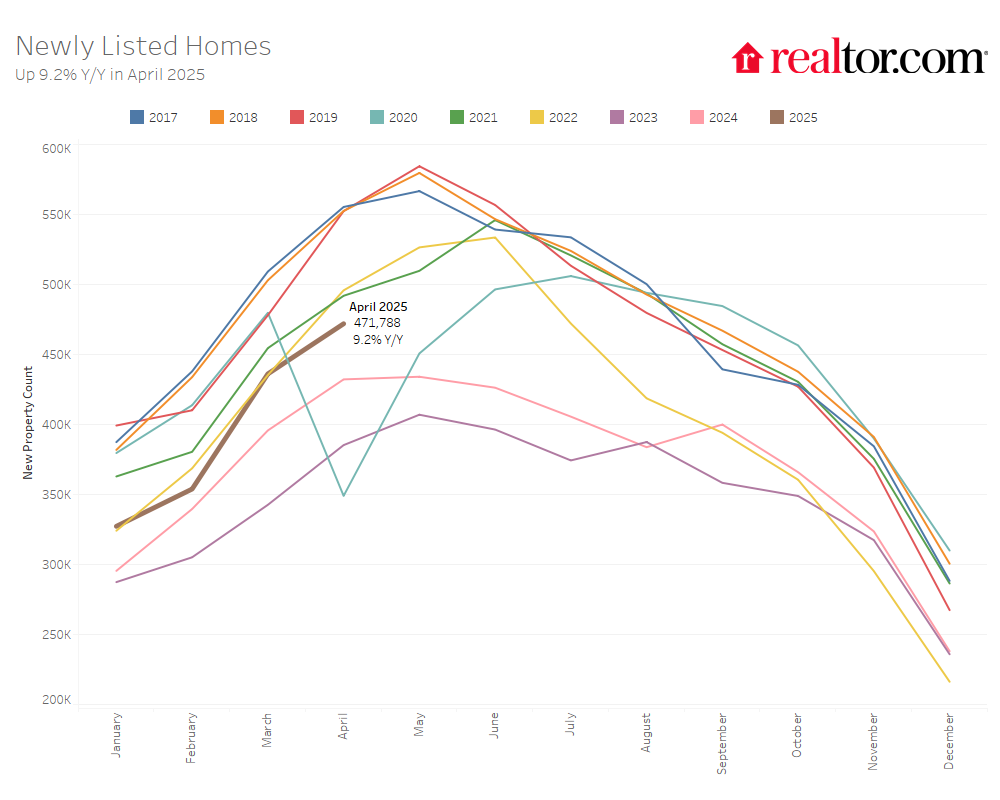

- Newly listed houses elevated 9.2% from a 12 months in the past.

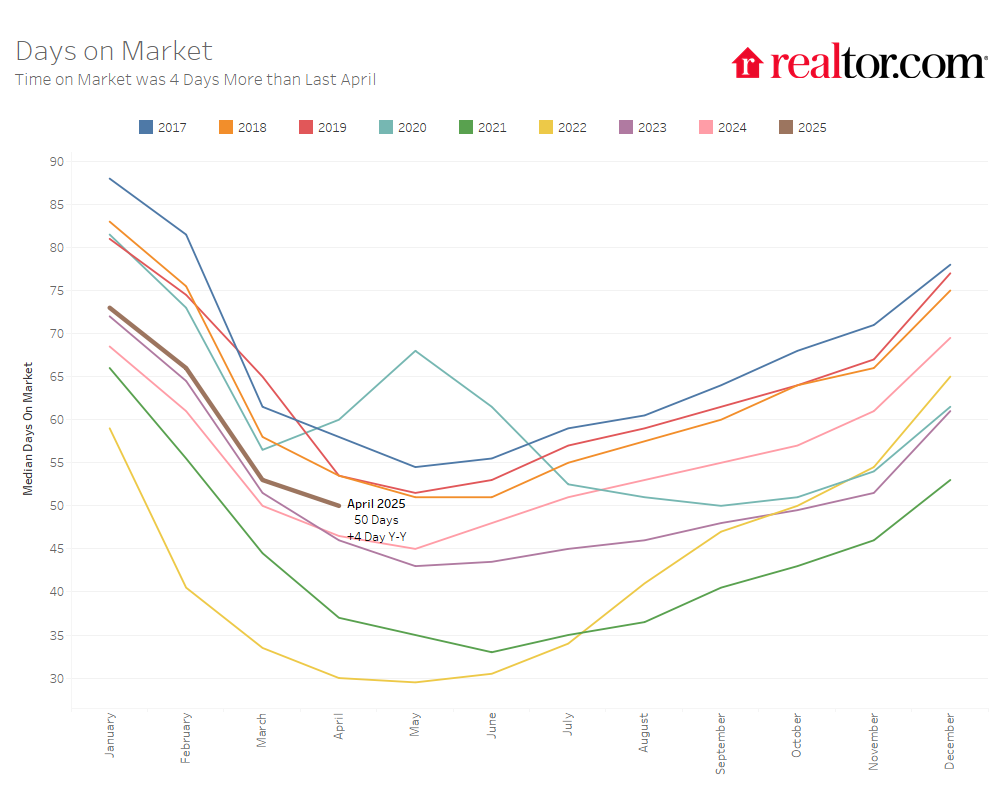

- Houses spent a median of fifty days available on the market, 4 greater than a 12 months in the past.

- The nationwide median checklist value for houses was $431,250, largely unchanged from final 12 months, whereas the value per sq. foot rose 1.1%, signaling modest residence worth development.

- The required revenue to afford the median residence rose by nearly $47,000 in comparison with 2019.

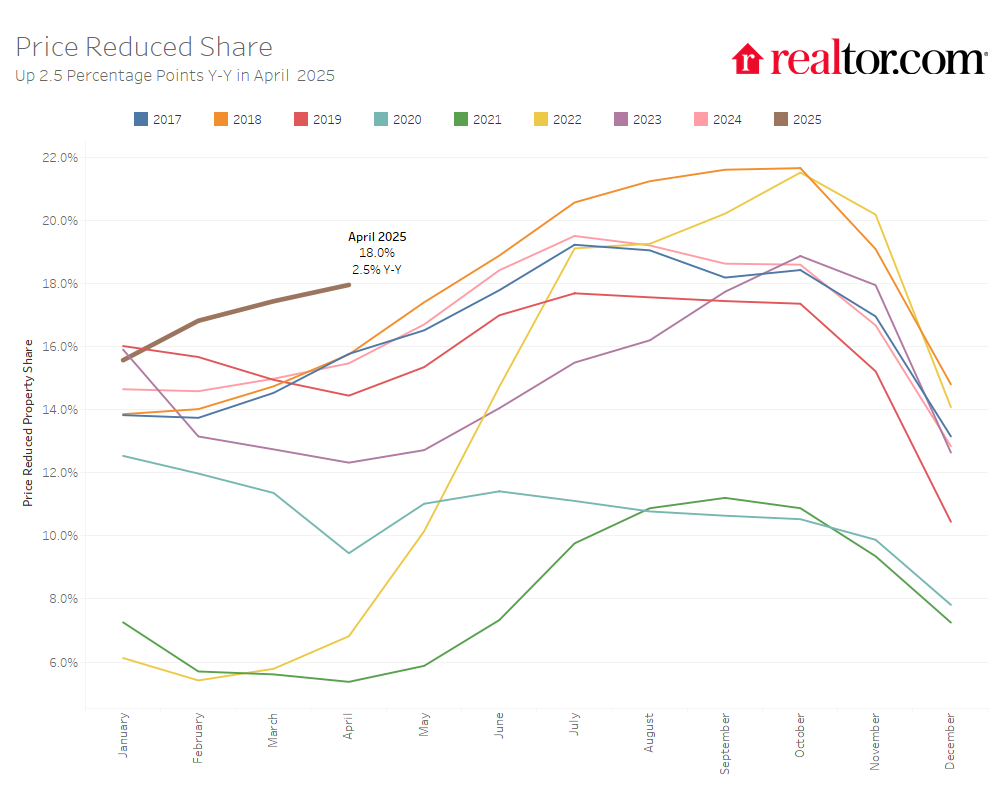

- 18.0% of listings noticed value reductions, the very best share for any April since a minimum of 2016.

In line with the Realtor.com® April housing information, the housing market supplied consumers extra choices, as stock continued to climb for the seventeenth straight month and new listings elevated throughout most areas. Houses are taking barely longer to promote than a 12 months in the past, although they’re nonetheless transferring quicker than earlier than the pandemic in lots of areas. Costs remained secure, however a rising share of sellers decreased their asking costs, reflecting mounting affordability pressures. After easing barely in March, mortgage charges rose once more in April, returning to final 12 months’s ranges amid market uncertainty surrounding authorities commerce and financial insurance policies—a shift that’s anticipated to gradual purchaser and vendor exercise within the months forward. Whereas the revenue wanted to buy a house has leveled off nationally over the previous 12 months, it stays considerably greater than earlier than the pandemic, underscoring the continuing problem of affordability whilst market situations step by step rebalance.

Patrons Acquire Choices as Stock Climbs Once more

Homebuyers discovered extra choices in April, because the variety of actively listed houses rose 30.6% in comparison with the identical time final 12 months. This marks the seventeenth consecutive month of year-over-year stock positive aspects and builds on March’s 28.5% enhance. For the primary time, the variety of houses on the market in April surpassed April 2020 ranges—a key pandemic benchmark. Regardless of this progress, energetic stock stays 16.3% beneath typical 2017–2019 ranges, signaling that the market nonetheless has floor to cowl. That mentioned, April’s positive aspects counsel the market is closing that hole extra rapidly than earlier than.

Whole residence itemizing stock, which incorporates each houses on the market and people beneath contract, additionally posted a stable 19.8% year-over-year enhance, sustaining its 17-month streak of development and surpassing April 2020 ranges as nicely.

Whereas stock was up, purchaser exercise was extra subdued. Pending residence gross sales—listings beneath contract—fell 3.2% year-over-year, marking a smaller decline than March’s 5.2% drop. Nevertheless, a late-April uptick in mortgage charges—reversing the downward development seen in March—may put renewed stress on demand. This enhance, pushed by market uncertainty round authorities commerce and financial coverage, introduced charges nearly again to the place they had been a 12 months in the past, doubtlessly discouraging some consumers who had been ready for additional declines. If greater borrowing prices persist, they could weigh on each pending gross sales and new listings as we transfer into the summer season season.

Newly listed houses supplied a vibrant spot, climbing 9.2% from final April. Nevertheless, this was a modest step again from March’s 10.2% enhance. Larger charges late within the month might have led some sellers to carry off, and itemizing exercise may ease additional if charge volatility continues.

The place Housing Stock Is Rising the Quickest

Stock elevated in all 4 main U.S. areas in April, although the tempo different:

- West: +41.7%

- South: +33.3%

- Midwest: +18.7%

- Northeast: +12.4%

In comparison with pre-pandemic norms, stock within the West (+4.8%) and South (+1.2%) has successfully recovered. However the Midwest (-44.0%) and Northeast (-55.7%) proceed to lag. These patterns echo building tendencies: the South led the nation in new housing begins in 2024, whereas the Northeast had the widest housing provide hole, per Realtor.com’s newest Provide Hole Report.

On the metro degree, all the 50 largest markets recorded year-over-year stock development. The sharpest will increase had been seen in:

- San Diego (+70.1%)

- Washington, D.C. (+69.3%)

- San Jose (+67.6%)

Nonetheless, most main metros stay beneath pre-pandemic stock ranges. Even so, 20 markets have now exceeded their 2017–2019 norms, up from 18 final month. Solely Southern and Western metros made this checklist, with Midwestern and Northeastern metros notably absent. Standouts embrace:

- Denver (+90.0%)

- Austin (+60.5%)

- Dallas (+53.4%)

Vendor Exercise Picked Up in Most Metros

Newly listed houses elevated throughout all 4 areas in April, led by:

- West: +11.7%

- Northeast: +10.2%

- South: +6.0%

- Midwest: +5.2%

Relative to pre-pandemic April months, the South is nearing a full restoration, with new listings simply 4.1% beneath historic norms. The Northeast continues to lag—down 33.2%—mirroring its persistent building shortfall.

Among the many 50 largest metros, 48 noticed a year-over-year enhance in new listings, up barely from 47 in March. Simply 8 metros surpassed pre-pandemic norms for brand new listings, together with Austin, San Antonio, and Dallas.

Metros with the strongest development in newly listed houses over the previous 12 months included:

- Denver (+24.7%)

- Phoenix (+22.9%)

- Boston (+20.1%)

Time on Market Edges Up in Many Areas

In April, the typical residence spent 50 days available on the market, which is 4 days longer than the identical time final 12 months. This marks the thirteenth straight month of houses taking longer to promote on a year-over-year foundation. Nonetheless, houses are transferring extra rapidly than they did earlier than the pandemic, spending 5 fewer days available on the market than the April 2017–2019 common.

Regional and Metro Developments: Time on Market Ticks Up

Three out of 4 areas noticed year-over-year will increase in time on market, reflecting broader cooling tendencies. The Northeast was the one exception, the place houses bought barely quicker than final 12 months, doubtless attributable to restricted stock within the area:

- South: +4 days

- West: +3 days

- Midwest: +1 day

- Northeast: -3 days

Relative to pre-pandemic norms, most areas are nonetheless seeing faster gross sales:

- West: 2 days slower

- South: 5 days quicker

- Midwest: 11 days quicker

- Northeast: 18 days quicker

Among the many 50 largest U.S. metro areas, 34 noticed houses linger longer than final 12 months. The largest slowdowns in time on market had been noticed in:

- Nashville (+16 days)

- Memphis (+8 days)

- Orlando (+8 days)

- Miami (+8 days)

A choose group of markets, together with Nashville, Portland, and Denver, at the moment are seeing listings sit longer than their pre-pandemic averages, indicating localized slowdowns whilst many areas stay quicker than historic norms.

Residence Costs Regular, however Sellers Are Extra Keen to Lower

In April, the nationwide median checklist value held at $431,250, nearly the identical as this time final 12 months (+0.3%). Whereas that top-line quantity is comparatively flat, the value per sq. foot—a gauge of residence values that accounts for smaller houses coming into the market—rose 1.1% year-over-year, indicating modest value development beneath the floor.

Since April 2019, the typical checklist value has climbed practically 37%, whereas value per sq. foot is up 54%. These long-term will increase have considerably affected affordability.

To afford a median-priced residence in April, a family wanted to earn about $114,000 per 12 months. That determine assumes:

- A 30-year mounted mortgage

- A 20% down cost

- Not more than 30% of your gross revenue going towards housing prices

Put merely, this implies you’d must earn about $9,500 per thirty days earlier than taxes to comfortably cowl the mortgage, property taxes, and insurance coverage on a typical residence.

In comparison with 2019, the required revenue has jumped by practically $47,000 (+70.1%), largely pushed by residence value appreciation and better mortgage charges. Nevertheless, over the previous 12 months, the required revenue has held comparatively regular, as mortgage charges and median costs have remained flat.

Regardless that general asking costs haven’t declined, extra sellers are making value cuts. In April, 18.0% of residence listings had value reductions—up 2.5 proportion factors from final 12 months. That is the highest April share in Realtor.com information going again to a minimum of 2016.

This development means that sellers are adjusting their expectations within the face of affordability challenges and weaker purchaser demand in some markets.

Regional Value Patterns: Flat or Falling in Most Areas

12 months-over-year modifications in median checklist costs by area had been:

- Northeast: +0.2%

- South: -0.4%

- West: -0.5%

- Midwest: -1.6%

When adjusting for altering residence sizes, value per sq. foot tells a extra constant story of development—besides within the South:

- Northeast: +4.2%

- West: +1.2%

- Midwest: +1.0%

- South: -0.1%

Amongst giant metros, the largest year-over-year value will increase had been:

- Windfall (+11.5%)

- Baltimore (+11.5%)

- Cleveland (7.0%)

Since 2019, the required revenue to purchase a house has risen sharply in lots of areas. The biggest jumps had been in:

- Memphis (+94.8%)

- Windfall (+92.8%)

- Las Vegas (+86.5%)

Metros with probably the most listings with value cuts, typically linked to slower demand, included:

- Phoenix (31.3% of listings)

- Tampa (29.3%)

- Jacksonville (27.6%)

April 2025 Regional Statistics

| Area | Lively Itemizing Depend YoY | New Itemizing Depend YoY | Median Itemizing Value YoY | Median Itemizing Value Per SF YoY | Median Days on Market Y-Y (Days) | Value-Diminished Share Y-Y (Proportion Factors) |

| Midwest | 18.7% | 5.2% | -1.6% | 1.0% | 1 | +1.3 pp |

| Northeast | 12.4% | 10.2% | 0.2% | 4.2% | -3 | +0.8 pp |

| South | 33.3% | 6.0% | -0.4% | -0.1% | 4 | +1.9 pp |

| West | 41.7% | 11.7% | -0.5% | 1.2% | 3 | +4.1 pp |

April 2025 Housing Overview of the 50 Largest Metros

| Metro Space | Median Itemizing Value | Median Itemizing Value YoY | Median Itemizing Value per Sq. Ft. YoY | Median Itemizing Value vs April 2019 | Required Revenue to Afford Median Residence | Required Revenue vs April 2019 |

| Atlanta-Sandy Springs-Roswell, Ga. | $412,470 | -0.8% | -1.3% | 26.9% | $109,034 | 57.7% |

| Austin-Spherical Rock-San Marcos, Texas | $525,000 | -5.9% | -5.1% | 41.9% | $138,781 | 76.3% |

| Baltimore-Columbia-Towson, Md. | $392,688 | 11.5% | 4.0% | 19.0% | $103,805 | 47.9% |

| Birmingham, Ala. | $299,900 | 1.5% | 0.8% | 18.8% | $79,277 | 47.6% |

| Boston-Cambridge-Newton, Mass.-N.H. | $878,000 | 0.9% | 1.6% | 46.4% | $232,095 | 81.9% |

| Buffalo-Cheektowaga, N.Y. | $280,000 | -1.7% | 1.2% | 31.8% | $74,017 | 63.8% |

| Charlotte-Harmony-Gastonia, N.C.-S.C. | $439,500 | 4.0% | 1.0% | 25.6% | $116,180 | 56.1% |

| Chicago-Naperville-Elgin, Sick.-Ind. | $372,450 | -4.4% | -0.5% | 9.8% | $98,455 | 36.4% |

| Cincinnati, Ohio-Ky.-Ind. | $347,725 | -7.3% | 2.3% | 23.8% | $91,919 | 53.8% |

| Cleveland, Ohio | $267,450 | 7.0% | 8.5% | 34.5% | $70,699 | 67.1% |

| Columbus, Ohio | $377,450 | -4.9% | 1.3% | 24.8% | $99,777 | 55.1% |

| Dallas-Fort Price-Arlington, Texas | $430,000 | -4.4% | -0.7% | 19.4% | $113,668 | 48.4% |

| Denver-Aurora-Centennial, Colo. | $599,450 | -4.1% | -1.1% | 14.5% | $158,462 | 42.2% |

| Detroit-Warren-Dearborn, Mich. | $253,575 | 1.4% | 1.8% | 1.3% | $67,031 | 25.8% |

| Grand Rapids-Wyoming-Kentwood, Mich. | $397,000 | -2.6% | 1.0% | 36.9% | $104,945 | 70.2% |

| Hartford-West Hartford-East Hartford, Conn. | $453,675 | 6.8% | 7.0% | 49.7% | $119,927 | 86.0% |

| Houston-Pasadena-The Woodlands, Texas | $369,900 | 0.2% | -0.6% | 14.7% | $97,781 | 42.5% |

| Indianapolis-Carmel-Greenwood, Ind. | $329,211 | -3.4% | -0.8% | 18.7% | $87,025 | 47.4% |

| Jacksonville, Fla. | $399,995 | -4.8% | -2.9% | 28.1% | $105,737 | 59.2% |

| Kansas Metropolis, Mo.-Kan. | $399,450 | -5.3% | 0.5% | 23.9% | $105,593 | 53.9% |

| Las Vegas-Henderson-North Las Vegas, Nev. | $475,000 | 0.0% | 0.9% | 50.1% | $125,564 | 86.5% |

| Los Angeles-Lengthy Seaside-Anaheim, Calif. | $1,195,000 | 0.3% | 1.4% | 49.7% | $315,892 | 86.0% |

| Louisville/Jefferson County, Ky.-Ind. | $324,950 | -0.6% | 1.9% | 16.2% | $85,899 | 44.4% |

| Memphis, Tenn.-Miss.-Ark. | $345,495 | 1.8% | 1.6% | 56.8% | $91,330 | 94.8% |

| Miami-Fort Lauderdale-West Palm Seaside, Fla. | $510,000 | -5.6% | -4.2% | 27.8% | $134,816 | 58.8% |

| Milwaukee-Waukesha, Wis. | $385,000 | 2.3% | 5.3% | 26.5% | $101,773 | 57.1% |

| Minneapolis-St. Paul-Bloomington, Minn.-Wis. | $447,400 | -0.5% | -0.2% | 20.4% | $118,268 | 49.6% |

| Nashville-Davidson-Murfreesboro-Franklin, Tenn. | $549,450 | -4.0% | -1.4% | 48.5% | $145,244 | 84.6% |

| New York-Newark-Jersey Metropolis, N.Y.-N.J. | $789,450 | 1.9% | -2.3% | 36.3% | $208,687 | 69.4% |

| Oklahoma Metropolis, Okla. | $322,255 | -2.3% | 0.4% | 27.4% | $85,186 | 58.3% |

| Orlando-Kissimmee-Sanford, Fla. | $425,000 | -3.4% | -2.1% | 35.8% | $112,347 | 68.7% |

| Philadelphia-Camden-Wilmington, Pa.-N.J.-Del.-Md. | $375,000 | 1.4% | 2.7% | 36.4% | $99,129 | 69.4% |

| Phoenix-Mesa-Chandler, Ariz. | $525,000 | -2.2% | -0.9% | 41.4% | $138,781 | 75.7% |

| Pittsburgh, Pa. | $243,724 | 0.5% | 1.6% | 33.2% | $64,427 | 65.6% |

| Portland-Vancouver-Hillsboro, Ore.-Wash. | $614,950 | 0.0% | -0.5% | 29.2% | $162,559 | 60.6% |

| Windfall-Warwick, R.I.-Mass. | $584,900 | 11.5% | 6.9% | 55.2% | $154,615 | 92.8% |

| Raleigh-Cary, N.C. | $451,245 | -0.5% | -0.3% | 22.0% | $119,284 | 51.6% |

| Richmond, Va. | $458,950 | 0.0% | 2.3% | 37.2% | $121,321 | 70.5% |

| Riverside-San Bernardino-Ontario, Calif. | $602,500 | 0.4% | 0.3% | 46.8% | $159,268 | 82.4% |

| Sacramento-Roseville-Folsom, Calif. | $633,570 | -2.5% | -1.5% | 30.1% | $167,481 | 61.7% |

| San Antonio-New Braunfels, Texas | $339,950 | -1.3% | -2.3% | 15.0% | $89,864 | 42.9% |

| San Diego-Chula Vista-Carlsbad, Calif. | $979,500 | -6.7% | -3.0% | 39.5% | $258,926 | 73.4% |

| San Francisco-Oakland-Fremont, Calif. | $995,000 | -3.1% | -5.6% | 5.0% | $263,023 | 30.5% |

| San Jose-Sunnyvale-Santa Clara, Calif. | $1,399,947 | -4.6% | -1.8% | 24.2% | $370,069 | 54.3% |

| Seattle-Tacoma-Bellevue, Wash. | $782,225 | 0.9% | 3.4% | 24.7% | $206,777 | 54.9% |

| St. Louis, Mo.-Sick. | $294,900 | 0.2% | -0.9% | 31.1% | $77,955 | 62.9% |

| Tampa-St. Petersburg-Clearwater, Fla. | $410,000 | -2.4% | -2.3% | 46.5% | $108,381 | 82.0% |

| Tucson, Ariz. | $396,133 | -3.2% | -0.7% | 32.7% | $104,716 | 64.9% |

| Virginia Seaside-Chesapeake-Norfolk, Va.-N.C. | $409,950 | 3.8% | 4.8% | 39.7% | $108,368 | 73.6% |

| Washington-Arlington-Alexandria, DC-Va.-Md.-W. Va. | $622,983 | -0.6% | -2.9% | 28.1% | $164,682 | 59.1% |

| Metro Space | Lively Itemizing Depend YoY | New Itemizing Depend YoY | Median Days on Market | Median Days on Market Y-Y (Days) | Value– Diminished Share | Value-Diminished Share Y-Y (Proportion Factors) |

| Atlanta-Sandy Springs-Roswell, Ga. | 45.2% | 8.8% | 46 | 7 | 20.8% | 3.1 pp |

| Austin-Spherical Rock-San Marcos, Texas | 24.5% | -0.6% | 44 | 2 | 25.9% | 1.2 pp |

| Baltimore-Columbia-Towson, Md. | 47.7% | 11.3% | 29 | -7 | 13.4% | 1.4 pp |

| Birmingham, Ala. | 18.2% | -1.9% | 50 | 4 | 16.1% | 1.4 pp |

| Boston-Cambridge-Newton, Mass.-N.H. | 25.7% | 20.1% | 25 | 1 | 12.1% | 1.7 pp |

| Buffalo-Cheektowaga, N.Y. | 3.2% | 8.4% | 35 | 1 | 6.5% | 1.2 pp |

| Charlotte-Harmony-Gastonia, N.C.-S.C. | 53.0% | 17.9% | 42 | 5 | 21.1% | 4.2 pp |

| Chicago-Naperville-Elgin, Sick.-Ind. | 11.4% | 1.9% | 33 | -1 | 10.4% | 1.8 pp |

| Cincinnati, Ohio-Ky.-Ind. | 24.0% | 9.6% | 34 | 3 | 13.2% | 2.5 pp |

| Cleveland, Ohio | 21.0% | 3.6% | 38 | -2 | 13.0% | 2.1 pp |

| Columbus, Ohio | 37.9% | 7.5% | 31 | 6 | 18.8% | 3.6 pp |

| Dallas-Fort Price-Arlington, Texas | 42.8% | 11.1% | 43 | 3 | 25.8% | 4.1 pp |

| Denver-Aurora-Centennial, Colo. | 65.0% | 24.7% | 36 | 4 | 27.2% | 6.1 pp |

| Detroit-Warren-Dearborn, Mich. | 16.7% | 10.6% | 37 | -3 | 12.6% | 2.7 pp |

| Grand Rapids-Wyoming-Kentwood, Mich. | 15.4% | -3.6% | 33 | 2 | 9.1% | -0.3 pp |

| Hartford-West Hartford-East Hartford, Conn. | 15.2% | 10.2% | 30 | -1 | 6.7% | 1.1 pp |

| Houston-Pasadena-The Woodlands, Texas | 33.9% | 10.7% | 44 | 1 | 19.2% | 1.1 pp |

| Indianapolis-Carmel-Greenwood, Ind. | 19.7% | 7.5% | 40 | 2 | 19.8% | 1.7 pp |

| Jacksonville, Fla. | 35.2% | 0.4% | 57 | 7 | 27.6% | 2.7 pp |

| Kansas Metropolis, Mo.-Kan. | 11.8% | 11.1% | 47 | 0 | 12.6% | 0.5 pp |

| Las Vegas-Henderson-North Las Vegas, Nev. | 60.7% | 18.2% | 44 | 5 | 21.4% | 7.5 pp |

| Los Angeles-Lengthy Seaside-Anaheim, Calif. | 54.6% | 8.3% | 44 | 5 | 14.3% | 5.6 pp |

| Louisville/Jefferson County, Ky.-Ind. | 22.9% | 10.5% | 39 | -1 | 14.7% | 1.0 pp |

| Memphis, Tenn.-Miss.-Ark. | 30.8% | -7.6% | 56 | 8 | 20.6% | 0.4 pp |

| Miami-Fort Lauderdale-West Palm Seaside, Fla. | 40.7% | -1.0% | 72 | 8 | 20.1% | 1.2 pp |

| Milwaukee-Waukesha, Wis. | 2.3% | 5.2% | 30 | -1 | 8.7% | 1.8 pp |

| Minneapolis-St. Paul-Bloomington, Minn.-Wis. | 8.9% | 8.4% | 33 | -3 | 10.6% | 0.0 pp |

| Nashville-Davidson-Murfreesboro-Franklin, Tenn. | 34.3% | 4.7% | 47 | 16 | 18.8% | -0.5 pp |

| New York-Newark-Jersey Metropolis, N.Y.-N.J. | 3.2% | 3.3% | 45 | -1 | 7.6% | 0.6 pp |

| Oklahoma Metropolis, Okla. | 30.0% | -0.9% | 43 | 2 | 18.4% | 0.4 pp |

| Orlando-Kissimmee-Sanford, Fla. | 44.7% | 5.3% | 62 | 8 | 23.4% | 2.8 pp |

| Philadelphia-Camden-Wilmington, Pa.-N.J.-Del.-Md. | 18.2% | 6.2% | 35 | -5 | 12.6% | 1.2 pp |

| Phoenix-Mesa-Chandler, Ariz. | 33.3% | 22.9% | 52 | -3 | 31.3% | 7.6 pp |

| Pittsburgh, Pa. | 16.8% | 8.9% | 47 | -5 | 15.7% | 2.4 pp |

| Portland-Vancouver-Hillsboro, Ore.-Wash. | 30.6% | 8.2% | 44 | 5 | 23.3% | 2.5 pp |

| Windfall-Warwick, R.I.-Mass. | 33.9% | 10.2% | 29 | 0 | 8.2% | 1.5 pp |

| Raleigh-Cary, N.C. | 58.2% | 16.2% | 43 | 5 | 20.1% | 6.6 pp |

| Richmond, Va. | 20.6% | 12.9% | 36 | -5 | 9.9% | 1.5 pp |

| Riverside-San Bernardino-Ontario, Calif. | 52.4% | 12.6% | 52 | 7 | 18.3% | 4.3 pp |

| Sacramento-Roseville-Folsom, Calif. | 49.6% | 13.1% | 38 | 6 | 17.9% | 3.3 pp |

| San Antonio-New Braunfels, Texas | 20.1% | 9.5% | 58 | 4 | 25.6% | 2.4 pp |

| San Diego-Chula Vista-Carlsbad, Calif. | 70.1% | 14.4% | 37 | 4 | 17.8% | 5.9 pp |

| San Francisco-Oakland-Fremont, Calif. | 42.6% | 5.5% | 33 | 6 | 13.4% | 4.1 pp |

| San Jose-Sunnyvale-Santa Clara, Calif. | 67.6% | 2.4% | 24 | 3 | 12.0% | 4.3 pp |

| Seattle-Tacoma-Bellevue, Wash. | 50.1% | 7.5% | 30 | 2 | 14.4% | 5.6 pp |

| St. Louis, Mo.-Sick. | 16.8% | 0.6% | 39 | 4 | 13.5% | 1.5 pp |

| Tampa-St. Petersburg-Clearwater, Fla. | 32.1% | 6.0% | 58 | 6 | 29.3% | 1.8 pp |

| Tucson, Ariz. | 56.5% | 14.9% | 51 | 6 | 23.5% | 4.6 pp |

| Virginia Seaside-Chesapeake-Norfolk, Va.-N.C. | 32.1% | 9.4% | 35 | 3 | 16.0% | 2.2 pp |

| Washington-Arlington-Alexandria, DC-Va.-Md.-W. Va. | 69.3% | 16.1% | 25 | -5 | 13.8% | 3.6 pp |

Methodology

Realtor.com housing information as of April 2025. Listings embrace the energetic stock of present single-family houses and condos/townhomes/row houses/co-ops for the given degree of geography on Realtor.com; new building is excluded except listed by way of an MLS that gives itemizing information to Realtor.com. Realtor.com information historical past goes again to July 2016. The 50 largest U.S. metropolitan areas as outlined by the Workplace of Administration and Funds (OMB-202301) and Claritas 2025 estimates of family counts.

Starting with this month’s report, we now have transitioned to a revised nationwide pending residence gross sales information sequence that applies enhanced cleansing strategies to enhance consistency and accuracy over time. Whereas the insights and commentary on this report replicate the brand new sequence, the downloadable information stays primarily based on our legacy automated pipeline. Consequently, there could also be slight variations between the report figures and people within the nationwide obtain file as we transition.

With the discharge of its January 2025 housing tendencies report, Realtor.com® has restated information factors for some earlier months. On account of these modifications, a number of the information launched since January 2025 won’t be immediately comparable with earlier information releases (information downloaded earlier than January 2025) and Realtor.com® economics analysis studies.