What a distinction a 12 months makes – within the 2022 version of Tendencies® within the Lodge Business, we wrote that main markets have been nonetheless attracting builders and that new provide development among the many nation’s 65 main markets was anticipated to file an annual achieve of 1.7%, which is above the long-run common of 1.5%. Nonetheless, over the previous 12 months, the market circumstances have modified with rising building prices, rising financing prices, much less financing choices attributable to the latest turmoil within the banking trade, and market uncertainty coming to the forefront, together with the restoration from the COVID-19 pandemic nonetheless enjoying an element.

The price of building supplies, labor and land has been rising steadily in recent times throughout the nation. Relying on the property’s particular location, class and franchise, resort building prices have elevated between 10% and 20% in most markets just lately, which is chopping into the developer’s revenue for a given growth. With that mentioned, it seems building prices might have peaked, and going ahead, extra typical, inflationary degree will increase in building prices are anticipated within the near-term.

Financing prices have risen over the previous 12 months and up to date turmoil within the banking trade attributable to the collapse of Silvergate Financial institution, Silicon Valley Financial institution, and Signature Financial institution are additionally making it a problem for builders to safe financing for brand new initiatives. The Federal Reserve started rate of interest hikes in March 2022, making an attempt to curb inflation. As of the date of this publication, CBRE is forecasting rates of interest to peak in mid-2023 and the Fed may start chopping rates of interest later in 2023. Certainty on the rate of interest outlook will present some stability for capital markets exercise as soon as that happens. Nonetheless, the Fed’s insurance policies might provoke a recession in 2023 or 2024 – CBRE’s financial forecast as of March 2023 calls for 2 consecutive quarters of unfavorable GDP development over the past half of 2023. If a recession involves fruition, there may be uncertainty relating to the magnitude of the recession and the way lengthy it is going to final.

On account of all these components, it has been troublesome for resort builders to determine possible resort developments. The provision development of latest resort rooms decreased in 2020 by means of 2022 because the resort market confronted challenges from COVID-19 and the restoration from the unprecedented pandemic. With the beforehand famous headwinds the market is presently dealing with, this pattern is more likely to proceed over the following a number of years.

Wanting again, from 2016-2019, the common annual fee of resort room provide development throughout the USA was 1.8% in contrast with the common annual fee of room night time demand development of 1.9%. New provide development dipped to 1.2% in 2020, 1.2% in 2021 and 0.5% in 2022. The February 2023 version of CBRE’s Lodge Horizons® initiatives new provide development to rise above the 2022 degree improve at a median fee above 1% for the following three years. This tempo is nicely beneath the quantity of latest provide development skilled earlier than the COVID-19 pandemic, and fewer than the two.5% tempo of demand development over the following three years.

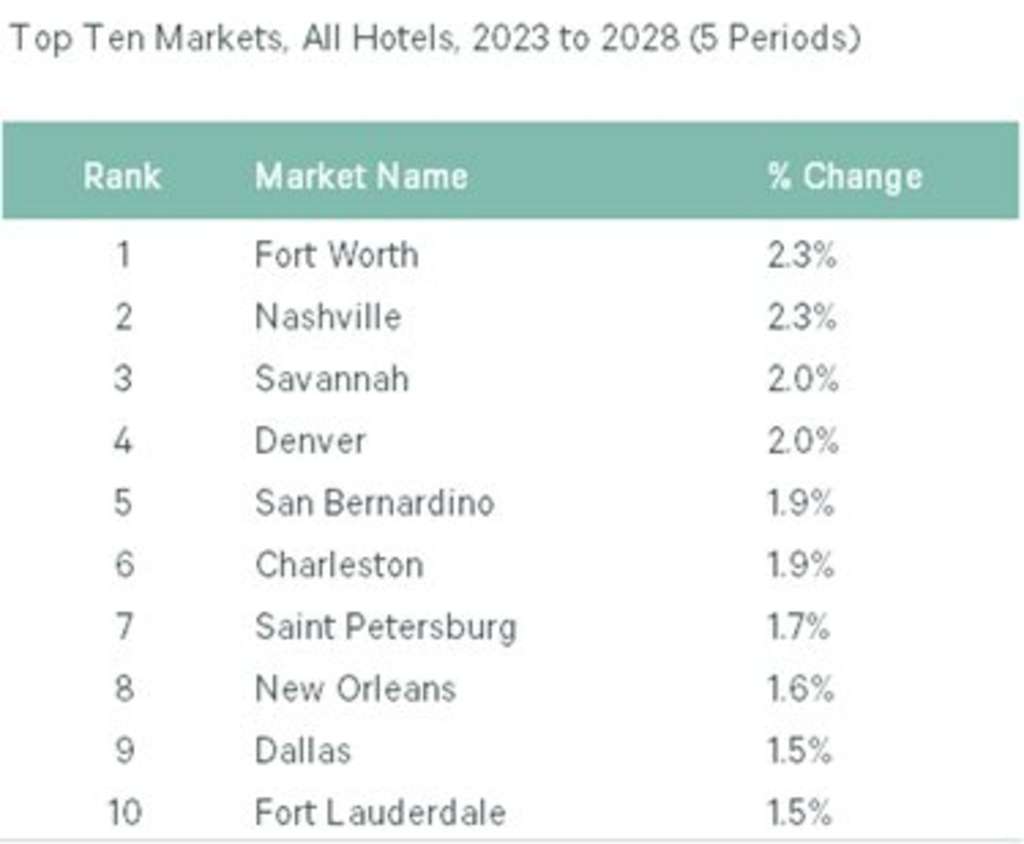

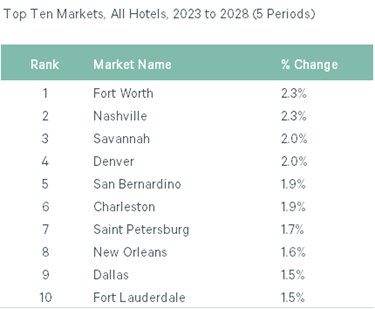

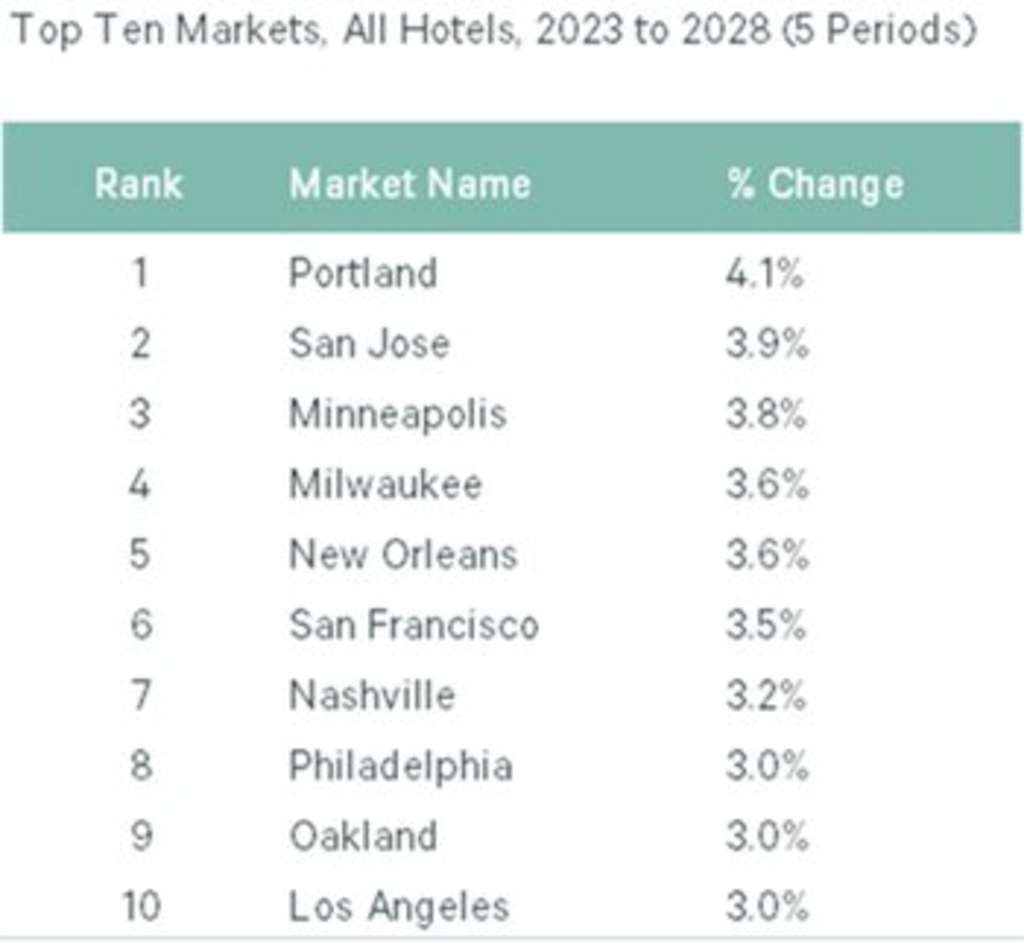

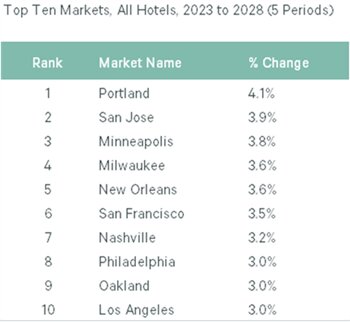

These provide and demand development fee figures are nationwide figures, and the influence of slower provide development is extra pronounced on a market degree. The next two lists rank the Prime 10 markets for forecasted new provide development and room night time demand development over the following 5 years.

— Supply: Supply: CBRE Lodges Analysis, This autumn 2022.

— Supply: Supply: CBRE Lodges Analysis, This autumn 2022.

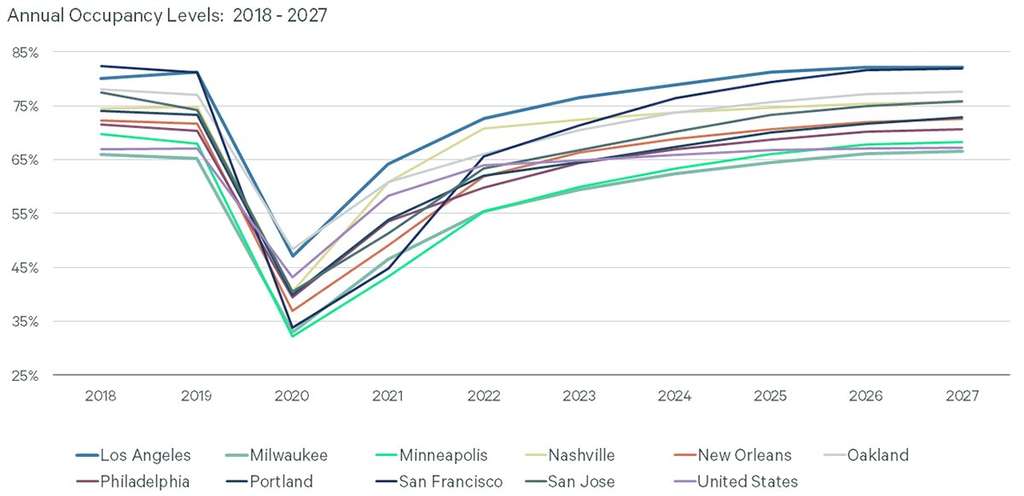

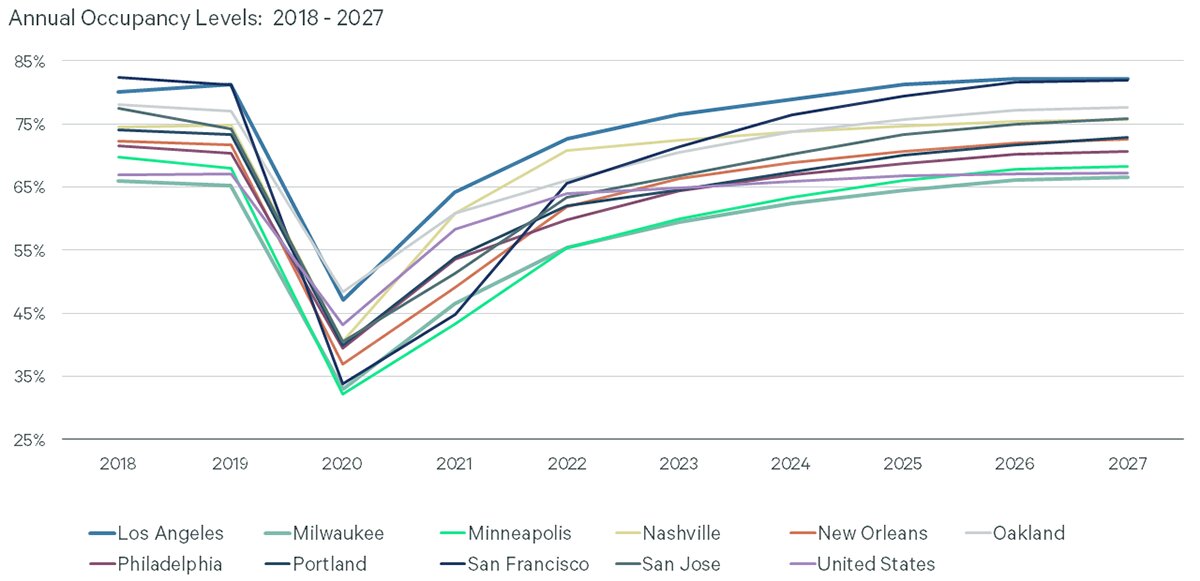

As is illustrated, solely two markets (New Orleans and Nashville) seem in each lists. Not shocking, as is proven within the following illustration, all 10 of the highest demand development markets are forecasted to expertise robust occupancy beneficial properties over the following 5 years, nicely above the occupancy development charges forecasted for the USA as a complete, which is projected to roughly degree out starting in 2024.

— Supply: Supply: CBRE Lodges Analysis, This autumn 2022.

The discount in new resort provide development may trigger a number of outcomes for the resort market, together with larger occupancy charges, rising room charges for current accommodations, and repositioning alternatives for older, inferior accommodations. If precise demand development charges exceed what’s forecasted in our fashions, the resort market may very well be dealing with a resort room provide scarcity, which might gas the expansion in occupancy charges and room charges. This will likely be a welcomed reprieve for the operators of many current accommodations which are pursuing larger occupancy charges, nearer to pre-COVID-19 ranges. With that mentioned, franchisors and market forces will seemingly place larger property enchancment plan necessities on current accommodations to justify larger charges and keep a aggressive benefit within the wake of decrease resort provide development in lots of markets. Additional, speculative resort builders banking on a stronger than anticipated restoration might profit from the gamble if the market outperforms expectations.

With the downturn from COVID-19 largely within the rearview mirror, an obvious moderation of building prices, and rate of interest will increase more likely to peak in 2023, we await the impacts from the Fed’s insurance policies to see if a recession happens and to what extent the potential recession impacts the general financial system and the resort market extra particularly. As soon as that turns into clearer, we may have a greater concept of how the decreased new resort provide will truly influence the resort market. As all the time, we are going to proceed to replace our forecasts and fashions as we obtain new information factors.