Open banking, which permits banks to share buyer information consensually with fintechs, is believed to be a game-changer for Nigeria’s monetary area. But the nation’s banking regulator, the Central Financial institution of Nigeria, is transferring slowly on its adoption.

Three years in the past, Nigeria’s Central Financial institution released the first draft of a regulatory framework for open banking. It was a pivotal second, and Nigeria loved the privilege of changing into the first African country to adopt the follow final yr.

It was commendable work from a regulator that’s usually on the receiving finish of criticism from the general public. But, months after transferring rapidly to undertake a framework, the apex financial institution has stalled on introducing a much-needed commonplace, protecting open banking in idea.

A typical will ideally create a uniform manner of transferring information via APIs and a public register of all of the contributors in open banking. Requirements are essential. For instance, earlier than the IBM commonplace, the private pc trade operated a number of person interfaces, making PC components very costly and out of attain for most individuals.

The IBM commonplace helped create the uniformity that the trendy PC trade was constructed on. Open banking wants this uniformity and the CBN’s obvious lack of urgency in direction of creating this commonplace dangers delaying a pivotal step in direction of monetary inclusion.

How can open banking change Nigeria?

Take lending for instance. Loans contribute considerably to the earnings of monetary establishments, and to make sure that they’re repaid, banks wish to have information factors on the purchasers to make knowledgeable lending choices. Up to now, bank-led lending has resulted in low credit score penetration, with as a lot as 70% of checking account holders locked out from accessible credit score.

In the previous couple of years, a number of fintechs have entered the credit score market to repair this regardless of having restricted information. The end result has been a mixed bag of sub-prime loans and predatory collection methods.

With open banking, lending fintechs would obtain information (transaction historical past, consumption patterns) from banks—there are a minimum of 120 million bank customers in Nigeria—to evaluate creditworthiness and likewise assist create a much-needed credit score rating for Nigerians.

Fintechs can even create new kinds of personalised monetary merchandise backed by information, as Nigerian banks are usually not incentivised to innovate given that almost all of their earnings come from non-banking sources. In what was a report yr for earnings, most banks made cash from the devaluation of the naira last year, with minimal earnings from core banking pursuits or new merchandise.

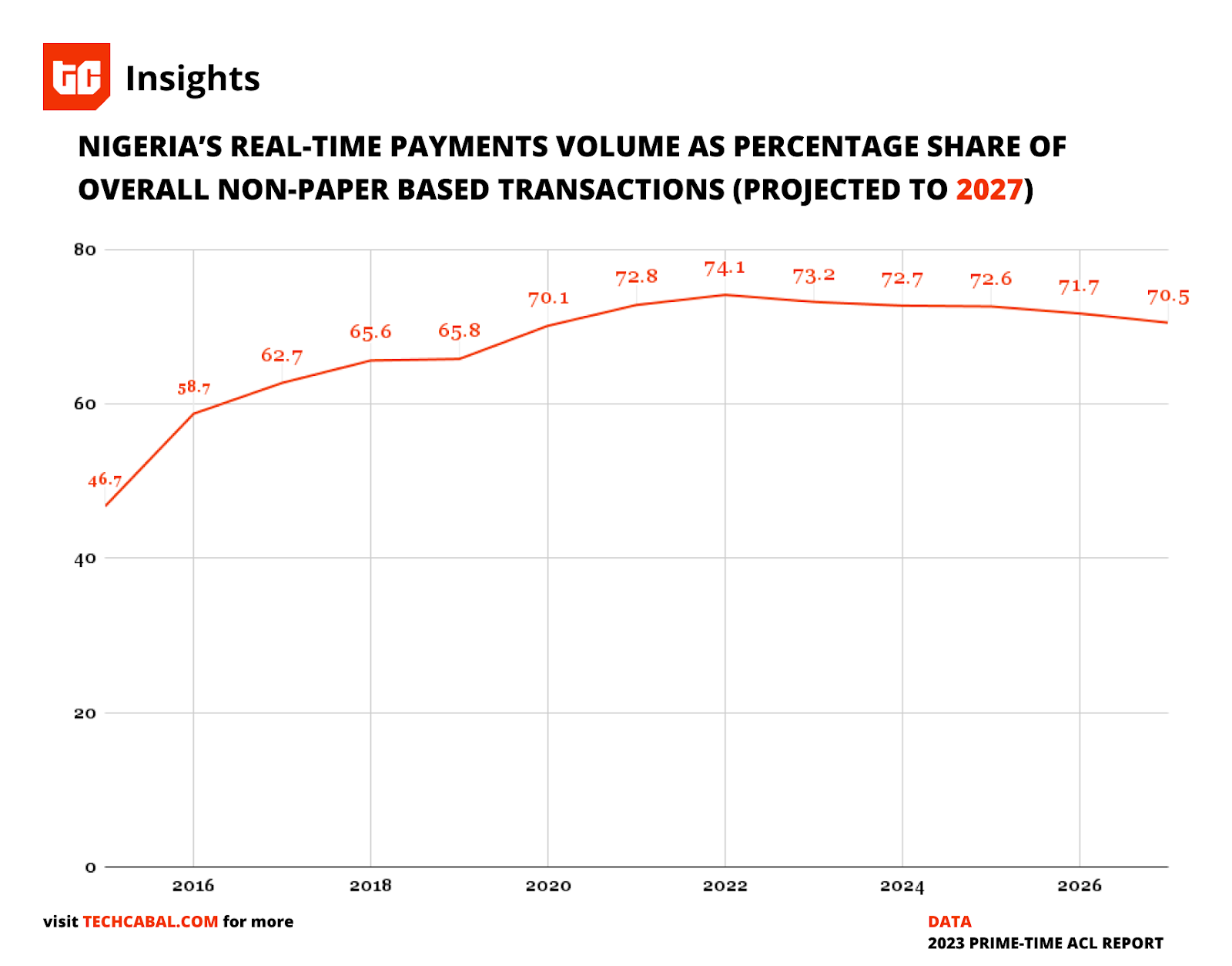

Nigeria is already a major market, with startups like Okra, Mono and Sew providing revolutionary options much like open banking resulting from demand. Actual-time funds, an important enabler, are booming. Final yr, Nigeria’s largest real-time fee infrastructure processed 9.6 billion transactions, in accordance with information seen by TechCabal.

Chart by Stephen Agwaibor/TC Insights

Ought to the CBN regulate open banking?

There are considerations that as a result of open banking depends on know-how, an ever-changing discipline, the CBN shouldn’t regulate it; as an alternative, it needs to be regulated by Nigeria’s information safety company, the Nigeria Information Safety Fee (NDPC), as information privateness is a foundational pillar of open banking.

“The central financial institution’s job is to implement insurance policies, not know-how,” stated David Peterside, the co-founder of Okra, an open banking startup.

The CBN’s tips from final yr targeted on two principal points; availability of know-how and safety. Peterside added that the CBN ought to as an alternative deal with making the banks and API suppliers companion as a result of the CBN’s regulatory burden would require banks to construct APIs, inflating prices for the banks. Massive British banks have spent more than £500 million on implementing open banking. With startups already offering related companies, banks can forgo this invoice.

However given the sensitivity of monetary info that will be shared, there isn’t any excellent manner that the CBN wouldn’t be concerned in a regulatory capability, stated Ikemesit Effiong, head of analysis at SBM Intelligence, a Lagos-based assume tank.

“Nigeria is a bank-led monetary system, so it won’t be uncommon for the CBN to provide out the rules. Nevertheless, violations shall be [the responsibility] of the info safety company,” Babatunde Obrimah, chief working officer of the Fintech Affiliation of Nigeria, advised TechCabal. He added that as a result of banks, fintechs, and cellular cash operators receive licences from the CBN, it’s the solely physique to manage them correctly, however interoperability have to be ensured.

What’s in it for the banks?

Proper now, there’s concern within the banking trade that the implementation of open banking would inevitably result in extra competitors. “It’s the identical pie that everybody is consuming out of, and also you don’t need anybody to eat into your half,” is how an trade insider places it.

That is, nevertheless, an unfounded concern as a result of most Nigerians use legacy banks and fintechs, Effiong stated. An analogous instance of person inertia is how the Nigerian Communications Fee (NCC) launched SIM porting a decade in the past, permitting clients to change community suppliers simply, however less than 2% of customers have ported since.

Income sharing, the prospect of mergers and acquisitions, and the CBN’s backing are a few of the methods banks will be incentivised to share their buyer’s information, Nnamdi Ifechi-Fred, a digital financial system analyst at Stears, advised TechCabal.

Public consciousness can spur the CBN

Public consciousness of the advantages of open banking can spur the CBN to finalise open banking. The UK turned considered one of Europe’s leaders in open banking by growing consciousness of the advantages of open banking. Inside two years, 11% of British consumers had been energetic customers of open banking.

Since India’s apex financial institution launched the Account Aggregator (AA) framework, which facilitates safe monetary information sharing by way of APIs, about 60% of Indian businesses see open banking as a gateway to buying consumer-consented information. It has now grow to be a staple in India and is powering the subsequent stage of open banking—open finance.

This may be replicated in Nigeria, however the CBN’s lack of a uniform commonplace is severely halting this progress. Fintechs have already built-in and partnered with banks, however the present actuality of open banking can’t energy the size that will deliver change to Nigeria. Why is the CBN stalling?