A change in shopper behaviour and macroeconomic circumstances are main Nigerian banks to difficulty native playing cards like Verve to prospects, dumping worldwide card schemes like Visa and Mastercard.

Earlier than the COVID-19 pandemic, Nigerian fintechs came upon a straightforward buyer acquisition technique: issuing international debit playing cards. These playing cards, typically issued at no cost or subsequent to nothing, ensured fintech prospects might withdraw cash at ATMs, or pay at supermarkets. Giving prospects debit playing cards elevated spending, permitting fintechs to earn extra transaction charges.

“No common Nigerian was going to spend [their] cash out of your financial institution if they didn’t have your card,” a former banker who requested to not be named instructed TechCabal.

Nonetheless, COVID-19-related restrictions on in-person buying, a money crunch in Nigeria in 2023, and cash shortages at bank ATMs have modified these assumptions and decreased the reliance on card funds. They’ve additionally led to the rising reputation of financial institution transfers.

Fintech startups and banks are reevaluating their card operations in step with these new realities, and all Nigerian business banks, besides Warranty Belief Holding Firm (GTCO), now difficulty Verve, a card scheme operated by Nigerian funds unicorn Interswitch.

First Financial institution, Nigeria’s oldest financial institution, has issued Verve playing cards to over half of its card prospects, mentioned one individual with information of the matter.

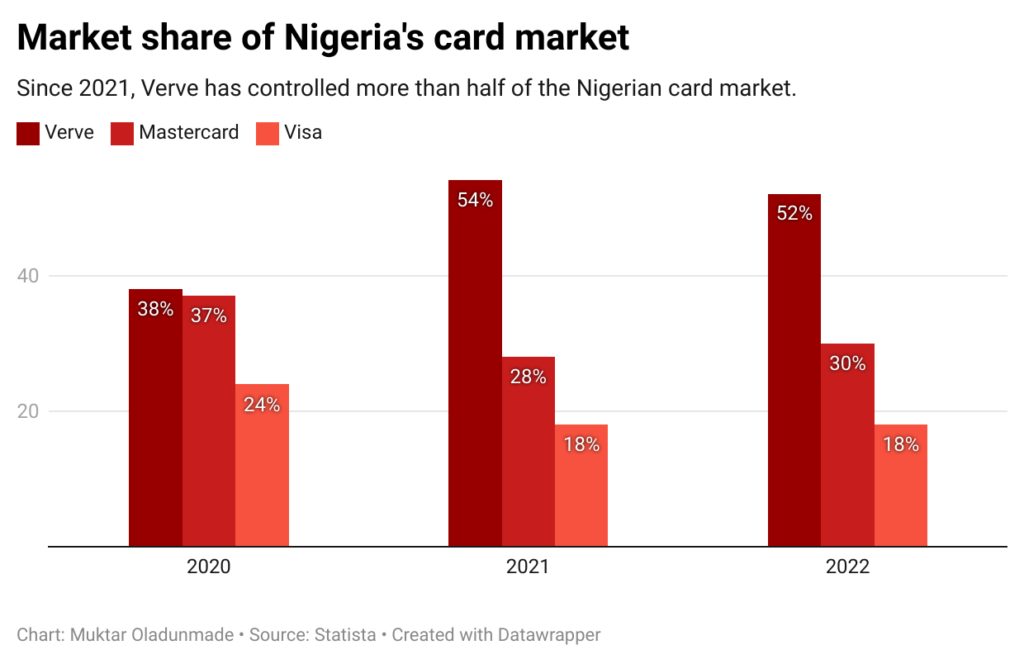

Chinese language-backed fintech OPay has issued 13 million Verve playing cards, whereas Moniepoint has issued about 4 million. For the reason that Covid pandemic led to 2021, Verve has managed 54% of the Nigerian card market.

Moniepoint declined to touch upon the figures.

Switching from the worldwide card schemes — which cost in USD — has turn out to be in style following the naira’s devaluation, making FX-denominated payments costlier.

Visa and Mastercard charges range and depend upon the monetary establishment’s measurement and area. The pricing technique of those worldwide card schemes can be sophisticated; Mastercard’s pricing information is a 300-page doc, mentioned one monetary trade skilled.

Monetary establishments should additionally meet necessities like a $2,000 month-to-month implementation cost, opening an offshore account, renewing their contracts yearly, and collateral that runs into hundreds of thousands of {dollars} mentioned three individuals with information of card operations. Worldwide card schemes additionally cost Nigerian banks a payment for logging disputes on their decision channels.

In addition they stop non-banks from connecting on to their card scheme, forcing fintechs to companion with business banks already on card schemes.

These complexities are driving the recognition of native alternate options like Verve and Afrigo regardless of heavy funding from Mastercard and Visa on the continent. Each firms have poured no less than $700 million into the continent’s fintech trade to remain related.

Visa and Mastercard didn’t reply to a request for feedback.

Moreover the cash, Verve and Afrigo make sense

The choice to modify to native card schemes can be related to prospects’ use of playing cards for native funds. With spending energy below strain due to inflation, the power to make world funds, which the massive card schemes supply, is beneficial to solely a small share of shoppers.

“Majority of fintech prospects use playing cards for POS transactions. They don’t seem to be buying on Amazon or on-line exterior the nation,” an worker at a Nigerian card scheme instructed TechCabal.

Nigeria can be going through its worst price of dwelling disaster in three a long time, decreasing buyer spend and inflicting a drop in interchange — the charges retailers pay for card processing — an issue for fintechs that want a excessive quantity of transactions to interrupt even with playing cards.

Underneath Godwin Emefiele, the Central Financial institution launched Afrigo, an area card scheme, and mentioned it might assist banks save prices. Fintechs, now firmly within the scope of regulators after a six-week ban on onboarding new prospects, are wanting to get within the regulator’s good books and see this as a straightforward route, in response to one individual accustomed to the talks.

The rise of the web switch fee technique has additionally meant that Nigerian fintechs are making merchandise that facilitate financial institution transfers. Stripe-owned Paystack has launched two pay-by-transfer merchandise in current months as financial institution transfers represented 58% of its transactions in Nigeria in 2023, up from 28% reported in 2022. These transfers supply higher margins than card funds because the a number of processors concerned in card funds are eradicated.

Moreover the swing in buyer behaviour, card operations require large scale to turn out to be worthwhile resulting from logistics, manufacturing, expertise, regulatory prices, and the danger of fraud.

These worldwide card schemes have thought of accumulating their charges in naira, a number of individuals accustomed to the talks instructed TechCabal.

However years of FX restrictions and $20 limits for world funds have made alternate options like digital playing cards in style and will imply prospects are detached concerning the change. So long as the playing cards work at a retailer, eating places, and POS stalls, it’s simply one other Monday.